In this article series, we explore regulatory trends shaping the future of personal investment advice powered by AI in the U.S. market. For more resources on this topic, explore our Investment AI blog section.

But first — one fundamental question:

Can an AI-powered investment advisory system operate in the United States while fully meeting fiduciary standards?

Why This Question Matters

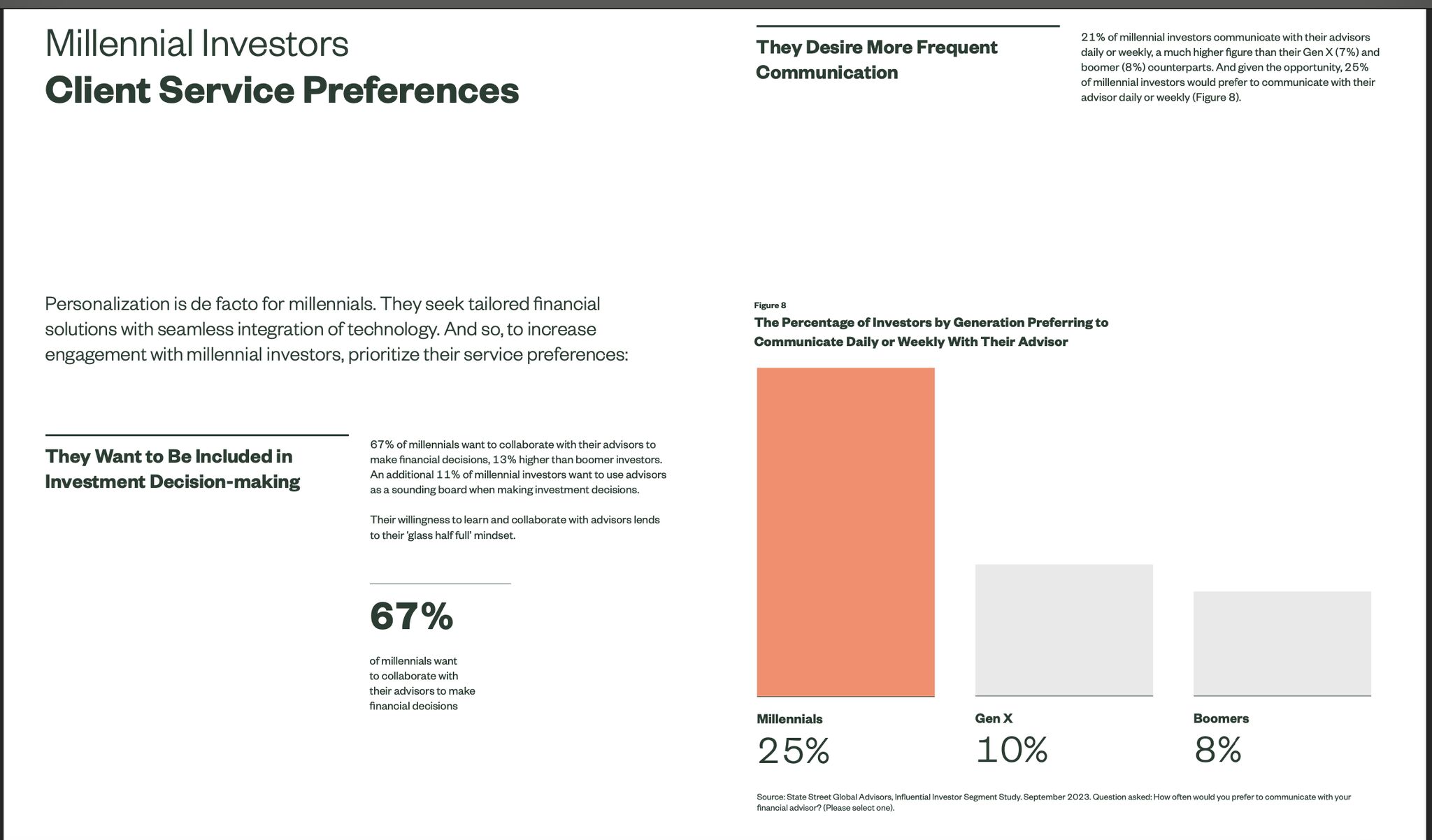

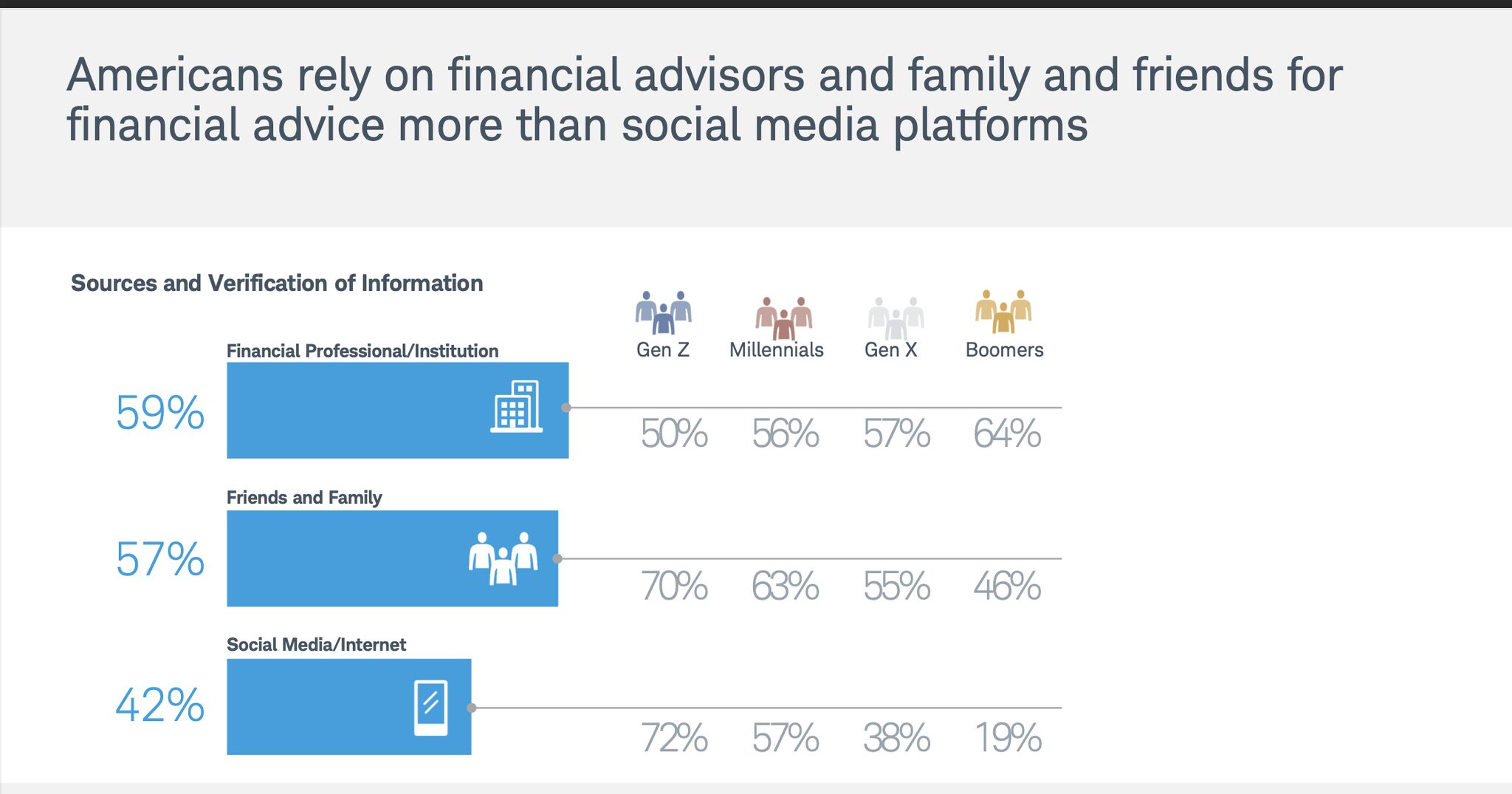

Recent reports from Charles Schwab (2024) and research by State Street highlight a growing gap: Investors increasingly demand personalized, high-quality advice, while simultaneously adopting fully digital platforms for their financial activities.

On one side, younger investors — especially Millennials and Gen Z — rely heavily on financial content circulating across social media platforms and subreddits. This content is easily accessible but often lacks credibility.

At the same time, as personal financial needs grow more complex, these same younger generations express a clear preference for professional, customized, and trustworthy advice — as long as it is fully digital and accessible.

Can AI Bridge This Gap?

AI-powered investment advisory solutions may serve as a bridge between younger investors and traditional fiduciary advisory models.

At the center of this question lies a core regulatory principle: Fiduciary Advice — where advisers act with full loyalty and prudence in the best interest of their clients.

SEC Fiduciary Duty — Key Obligations

According to the U.S. Securities and Exchange Commission (SEC), fiduciary duty includes:

- Providing advice that serves the client's sole interest

- Full transparency regarding conflicts of interest

- Full responsibility for managing the client relationship from beginning to end

This is not a marginal issue. As of 2024, more than $17 trillion in client assets are managed by fiduciary investment advisers in the U.S. (IAA data).

Where Does AI Fit Into the Fiduciary Framework?

In 2023, the SEC published a draft proposal stating that AI-powered advisory systems may still qualify as fiduciary advisers. As such, they would be subject to the same legal and ethical obligations that apply to human advisers.

Being "smart" is not enough — AI systems must be trustworthy, prudent, and transparent.

While this SEC draft was formally withdrawn on June 12, 2025, core fiduciary duties remain fully applicable to all investment advisers — regardless of whether advice is delivered by humans or AI-powered platforms.

The Current Reality

In practice, there are a handful of U.S.-licensed firms already offering AI-powered personal investment advice. However, this segment remains very small. The majority of retail investment advisory services in the U.S. continue to operate under traditional human-centered models.

Regulatory Planning Is Essential

In this evolving environment, thoughtful and comprehensive regulatory planning is no longer optional — it's a prerequisite for success.

As AI technology continues to advance and investor preferences shift toward digital-first solutions, firms that proactively address regulatory requirements will be best positioned to capture this emerging market opportunity while maintaining the highest standards of client protection.

References

- Schwab Modern Wealth Survey 2024 - https://www.aboutschwab.com/schwab-modern-wealth-survey-2024

- State Street Global Advisors: The 2024 Influential Investor Segment Study - https://www.ssga.com/us/en/intermediary/resources/practice-management/the-2024-influential-investor-segment-study

- Investment Adviser Association: 2025 Snapshot Report - https://www.investmentadviser.org/wp-content/uploads/2025/05/Snapshot2025.pdf